The market for specialty papers is continually changing due to demand for sustainable packaging solutions, evolving environmental regulations, new papermaking technologies, and new materials for paper and coatings.

The Future of Specialty Papers to 2030, a new report from Smithers, details these trends as well as the latest developments in biobased coatings and alternative fibers, e-commerce and more.

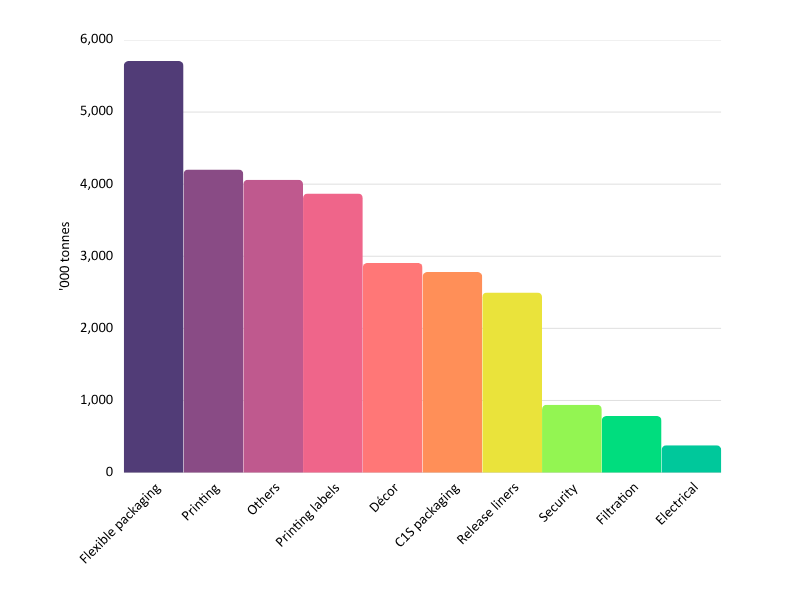

According to the new research, the global specialty papers market is predicted to be 28.2 million tonnes in 2025 and projected to grow to 31.3 million tonnes by 2030. This represents a compound annual growth rate (CAGR) of 2.1% for this five-year period. The largest categories of specialty papers are flexible packaging, printing papers, and printing labels, representing 49% of the 2025 market tonnage.

The Impact of Regulations

Sustainable packaging structures and the governing policies that support them are key drivers in changing the kinds of products that are made, how they are designed, which raw materials are utilized, and their disposition at the end of their lifecycle.

Non-recyclable film structures used in flexible packaging are being displaced by new barrier coated paper structures, which are recyclable. Also included is the requirement for recycled content in the package design. The objective is to reduce packaging waste that goes into landfills. Packaging companies that do not comply with the new regulations will pay a fee that supports the recycling infrastructure.

In the EU, a new regulation called the Packaging and Packaging Waste Regulation (PPWR) has been enacted to reduce packaging waste and promote recyclable alternatives. Revised in 2025, the new legislation replaced the Packaging and Packaging Waste Directive (PPWD). The PPWR imposes strict rules on packaging design, recycling, and waste reduction.

The legislation intends to transition all packaging to recyclable versions by 2030 in a cost-effective manner while reducing the use of virgin materials. When the producers of packaging start seeing the bottom-line impact of these new regulations, they will be forced to comply.

In the US, the regulations are not nearly as unified as the EU. Each individual state could enact their own EPR regulations if they so choose, driving different requirements and outcomes.

Over the next five years, flexible packaging will see a gradual shift away from petroleum-based films to paper-based structures for selected package types. The driving force for this transition is the end-of-life scenario for the package, and the regulations that address the requirements for the package to be recyclable, compostable, or both. Extended producer responsibility (EPR) is now in effect or being adopted on a gradual basis in the continents of Europe, Africa, Oceania, and North America.

New technologies

The latest technologies that impact specialty papers include new “Smart” controllers for advanced control algorithms. These are ideal for start-ups and shutdowns, in which steady-state control has not been established. Process optimization is also achievable with this methodology.

Artificial intelligence is making its capabilities known in areas such as packaging design, meeting administration, drafting of documents including interoffice emails, reports, even Board level presentations. The advancements in digital printing continue, with higher speeds, wider web widths, and higher print resolution. These advancements are helping to drive the cost per piece downward, making it far more competitive. The utilization of digital printing of labels and flexible packaging continues to trend upward. Curtain coating is being utilized to a greater degree to apply barrier coatings to papers, as it offers many competitive advantages.

Projected specialty paper sales by category, 2025

Source: Smithers

Source: Smithers